Department of Agriculture (USDA) are just provided for properties found in a qualifying rural area. Also, the private home mortgage insurance coverage requirement is generally dropped from standard loans when the loan-to-value ratio (LTV) is up to 80%. However for USDA and Federal Real Estate Administration (FHA) loans, you'll pay a variation of home mortgage insurance coverage for the life of the loan.

Your financial health will be carefully scrutinized throughout the underwriting procedure and before the home loan is provided or your application is rejected. You'll require to supply current paperwork to validate your work, earnings, assets, and debts. You might also be required to submit letters to explain things like employment gaps or to document presents you receive to help with the deposit or closing expenses.

Prevent any huge purchases, closing or opening brand-new accounts, and making uncommonly big withdrawals or deposits. what credit score do banks use for mortgages. As part of closing, the loan provider will need an appraisal to be finished on the home to verify its value. You'll likewise need to have a title search done on the property and protected lender's title insurance coverage and house owner's insurance coverage.

Lenders have ended up being more stringent with whom they want to loan cash in reaction to the pandemic and occurring economic recession. Minimum credit score requirements have increased, and lending institutions are holding debtors to greater requirements. For example, lenders are now confirming work prior to the loan is completed, Parker states.

A Biased View of What Are Current Interest Rates On Mortgages

Numerous states have fasted lane approval for the use of digital or mobile notaries, and virtual home tours, " drive-by" appraisals, and remote closings are ending up being more common. While many lenders have actually improved the logistics of approving home loans from another location, you may still experience hold-ups while doing so. All-time low home mortgage rates have caused a boom in refinancing as existing homeowners aim to conserve.

Spring is typically a hectic time for the property market, however with the shutdown, lots of purchasers had to put their home searching on pause. As these purchasers return to the marketplace, loan originators are ending up being even busier.

Due to the fact that individuals typically don't have enough cash available to purchase a house outright, they usually take out a loan when purchasing real estate. A bank or home loan lending institution consents to supply the funds, and the debtor consents to pay it back over a specific period of time, say thirty years.

Depending on where you live, you'll likely either sign a home loan or deed of trust when you secure a loan to buy your house. This file offers security for the loan that's evidenced by a promissory note, and it creates a lien on the home. Some states use home loans, while others utilize deeds of trust or a similarly-named document.

What Does Which Of The Following Is Not True About Reverse Annuity Mortgages? Do?

While many people call a house loan a "home loan" or "mortgage loan," it's actually the promissory note which contains the guarantee to repay the amount borrowed. Mortgages and deeds of trust usually include an acceleration stipulation. This provision lets the lending institution "accelerate" the loan (state the entire balance due) if you default by not making payments or otherwise break your loan arrangement, like stopping working to pay taxes or preserve the needed insurance.

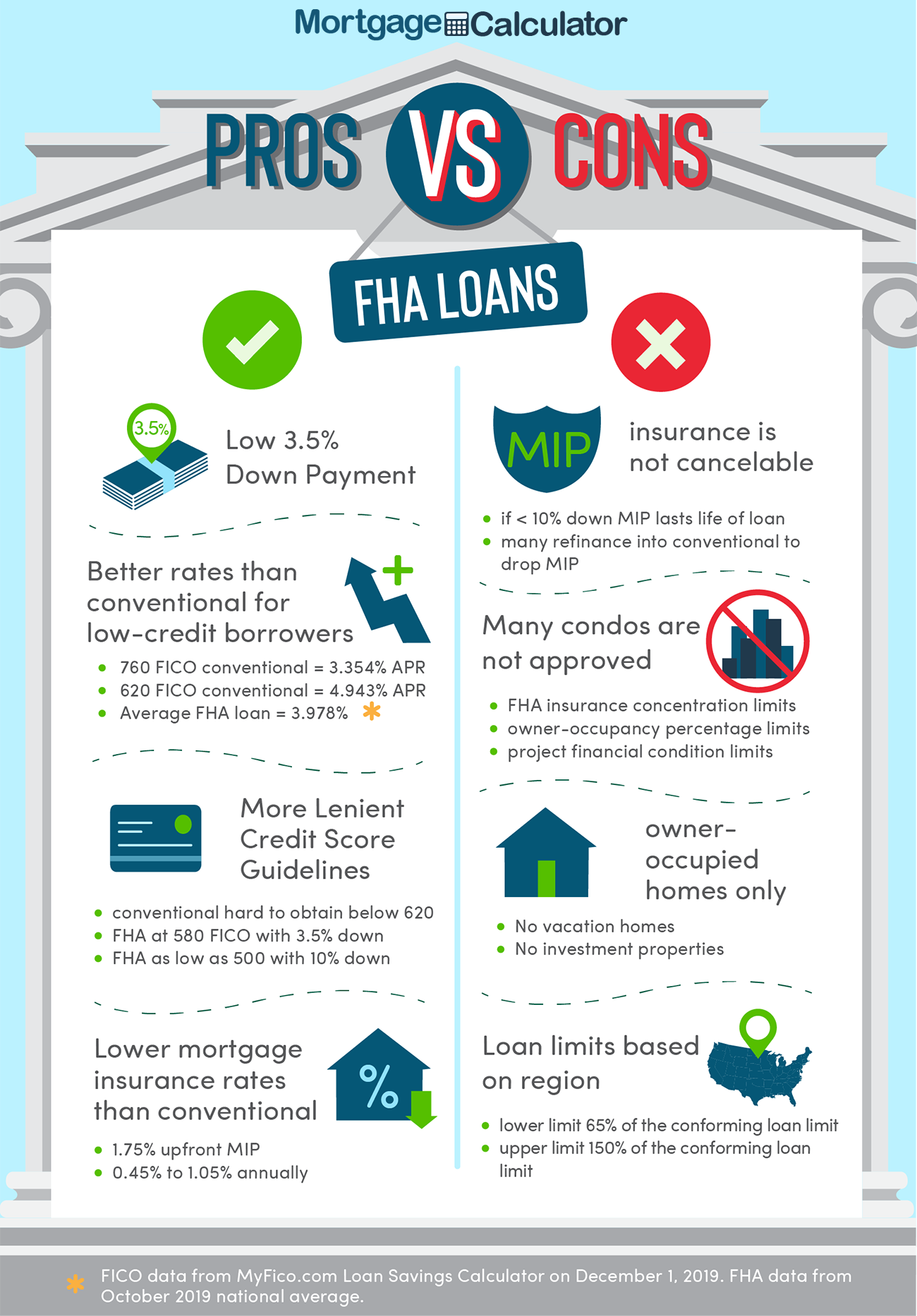

The majority of home loan customers get an FHA, VA, or a traditional loan. The Federal Housing Administration (FHA) guarantees FHA loans. If you default on the loan and your house isn't worth enough to totally repay the debt through a foreclosure sale, the FHA will compensate the lender for the loss. A customer with a low credit rating might wish to think about an FHA loan due to the fact that other loans typically wyndham timeshare for sale aren't available to those with bad credit.

Department of Veterans Affairs (VA) assurances. This type of loan is only offered to specific customers through VA-approved lending institutions. The guarantee means that the loan provider is secured versus loss if the customer fails to pay back the loan. A current or former military servicemember may desire to consider getting a VA loan, which might be the least pricey of all 3 loan types.

So, unlike federally insured loans, standard loans bring no warranties for the loan provider if you stop working to repay the loan. (Find out more about the distinction between traditional, FHA, and VA loans.) Homebuyers sometimes think that if a lender pre-qualifies them for a mortgage loan, they have actually been pre-approved for a home mortgage.

What Is The Current Libor Rate For Mortgages - Questions

Pre-qualifying for a loan is the first action in the home mortgage process. Typically, it's a pretty simple one. You can pre-qualify rapidly for a loan over the phone or Web (at no expense) by providing the lender with an introduction of your finances, including your income, possessions, and financial obligations. The lending institution then does an evaluation of the informationbased on only your wordand provides you a figure for the loan amount you can most likely get.

It is necessary to comprehend that the loan provider makes no assurance that you'll be authorized for this quantity. With a pre-approval, however, you supply the home loan lender with information on your earnings, possessions, and liabilities, and the lending institution verifies and evaluates that info. The pre-approval procedure is a much more involved procedure than getting pre-qualified for a loan.

You can then try to find a house at or below that rate level. As you may think, being a pre-approved buyer carries far more weight than being a pre-qualified purchaser when it pertains to making a deal to buy a home; when you find the house you want and make a deal, your deal isn't subject to obtaining funding.

Jointly, these products are called "PITI (who has the best interest rates on mortgages)." The "principal" is the quantity you obtained. For instance, expect you're purchasing a house that costs $300,000. You put 20% of the house's cost down ($ 60,000) so that you can avoid paying private home loan insurance (PMI), and you borrow $240,000. The primary amount is $240,000.

The Only Guide to How Do Lenders Make Money On Reverse Mortgages

The interest you pay is the cost of obtaining the principal. When you take out the home mortgage, you'll accept a rates of interest, which can be adjustable or repaired. The rate is revealed as a percentage: around 3% to 6% is basically basic, but the rate you'll get depends on your credit history, your income, properties, and liabilities.

Eventually, though, you'll pay mainly principal. When you own property, you have to pay property taxes. These taxes pay for schools, roads, parks, and so on. Sometimes, the lender establishes an escrow account to hold cash for paying taxes. The customer pays a portion of the taxes each month, which the loan provider locations in the escrow account.

The home timeshare exit team dave ramsey mortgage agreement will need you to have homeowners' insurance coverage on the residential or commercial property. Insurance payments are also typically escrowed. If you require more information about mortgages, are having difficulty deciding what loan type is best for your situations, or require other home-buying recommendations, consider calling a HUD-approved real estate counselor, a home mortgage loan provider, or a genuine estate attorney.