But they do need monetary therapy from a HUD-approved HECM counselor, which is some indication of just how complex they are. The building is not the principal residence of at least one enduring borrower. A nonborrowing partner may be able to continue to be in the home if particular qualification requirements are satisfied. The residence is no longer the debtor's principal home.

- After that, you'll require to either repay the funding or refinance it if you no longer desire a reverse home loan.

- A reverse home loan is a finance for house owners 62 and also up with large residence equity looking for more cash flow.

- A reverse home mortgage is a finance where you borrow an amount of cash versus the worth your residential or commercial property.

- If your estate or successors plan to sell the house or obtain funding to pay off the financing and also need more than one month, they might get a 90-day expansion from the lending institution by providing approved documents of their efforts.

- You must constantly weigh a reverse home mortgage versus various other options that do not entail additional debt later on in life.

Hong Kong Home Mortgage Firm, a federal government funded entity similar to that of Fannie Mae as well as Freddie Mac in the United States, gives credit history improvement solution to industrial financial institutions that originate reverse mortgage. Besides offering liquidity to the financial institutions by securitization, HKMC can provide assurance of reverse home mortgage principals up to a specific percent of the finance worth. Since 2016, reverse https://beterhbo.ning.com/profiles/blogs/exactly-how-the-federal-reserve-influences-home-mortgage-rates mortgage is offered to house-owners aged 55 or above from 10 various banks. Applicants can likewise enhance the car loan value by promising their in-the-money life insurance policies to the bank. In regards to making use of proceed, candidates are allowed to make one-off withdrawal to spend for home upkeep, medical and legal expenses, in addition to the monthly payout.

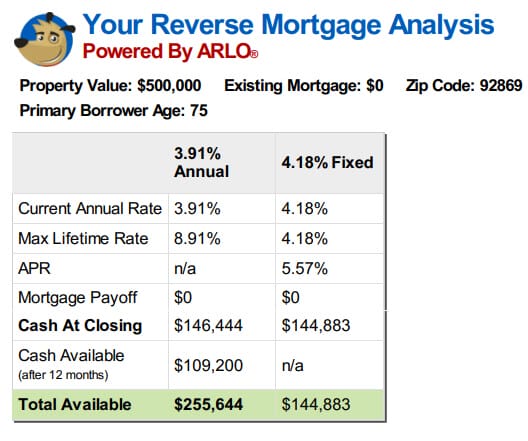

Requirements Of A Reverse Mortgage

Conversation with a loan provider concerning whether a reverse home mortgage is ideal for you. Your rates of interest will have an effect on just how much you qualify for. Since interest costs are contributed to your loan each month, the lower the interest rate, the extra you'll have the ability to borrow. Reverse home loans can be an excellent suggestion for seniors who require even more retired life revenue yet still wish to reside in their residences. Nevertheless, this could not be the very best choice for you if you intend to pass your house to your kids, or if you intend on vacating the home soon. If you have a HECM, which is backed by the federal government, your funding is thought about a non-recourse car loan, meaning you'll never ever owe greater than your residence deserves.

Guide To Reverse Home Mortgages

To be eligible, you need to be over the age of 60, own your very own house outright, or have a conventional home loan that can be paid off by the reverse home mortgage. The quantity you can access relies on your age and the worth of your home. The complete loan quantity, including gathered rate of interest, is repayable when you move permanently from your residence.

You have to be at least 62 years of ages, and you should either own your house complimentary and clear or have a considerable amount of equity (at least 50%). Debtors need to pay an origination cost, an up front home mortgage insurance policy costs, recurring home loan insurance coverage premiums, car loan maintenance costs, as well as passion. The federal government limitations how much lenders can charge for these things. If you are the last enduring debtor on the finance, the financing has to be paid within thirty days of the date of your death. If your estate or timeshare today beneficiaries plan to sell the home or obtain funding to repay the car loan as well as need greater than thirty day, they might obtain a 90-day extension from the lending institution by giving accepted documentation of their initiatives. As a reverse home mortgage debtor, you are required to live in the residence and also keep it.

If your spouse is not a co-borrower on your reverse home loan, after that they might need to pay off the finance as soon as you relocate or pass away. When it comes to whether they can stay in your home without settling, that relies on the timing of the HECM and also the timing of your marital relationship. If you pass away, and your successors wish to maintain the residence, they can refinance to a conventional mortgage, acquisition it for the quantity owed on the reverse home mortgage or 95% of the assessed value-- whichever is reduced. They can additionally market the residence and keep any type of remaining profits after the financing is settled or just sign the deed over to the lender. As soon as the property owners move, offer their house or die, the reverse mortgage is repaid.

There Are A Number Of Prices

When the reverse home mortgage agreement ends and also the consumer's home is marketed, the lender Learn more here will get the profits of the sale and also the customer can not be held liable for any debt over of this. Where the property sells for greater than the amount owed to the lending institution, the consumer or his estate will certainly get the added funds. It's important to have a plan to manage your reverse mortgage after you die. Paying off the financing can get made complex, depending on how much equity you have in your house and also whether you desire the house to stay in your household after your fatality. To additionally complicate points, you can not obtain all of your initial major restrictions in the first year when you pick a lump sum or a credit line.

As kept in mind earlier, the loan provider may call the lending due in any of the above-described scenarios. Reverse home loan lending institutions are commonly quick to begin a foreclosure after a default takes place. You can select to shield a portion of the ultimate internet sale profits of your home. When your lending is paid back, you're ensured to have this selected portion went back to you (as much as 50%). Read about the benefits and drawbacks of a reverse home loan to see if it is ideal for you.

Consider your current monetary circumstance as well as where you wish to be a few years later on. If you have actually already closed on a finance, remember you have up to 3 days to cancel by means of your right of rescission. It's important to keep in mind that a reverse home loan is still a financing and that the money you receive from it is ultimately your very own cash that's locked up in your home. Getting money from your home loan might appear also great to be true.